Retirement Roundup - March 28, 2025

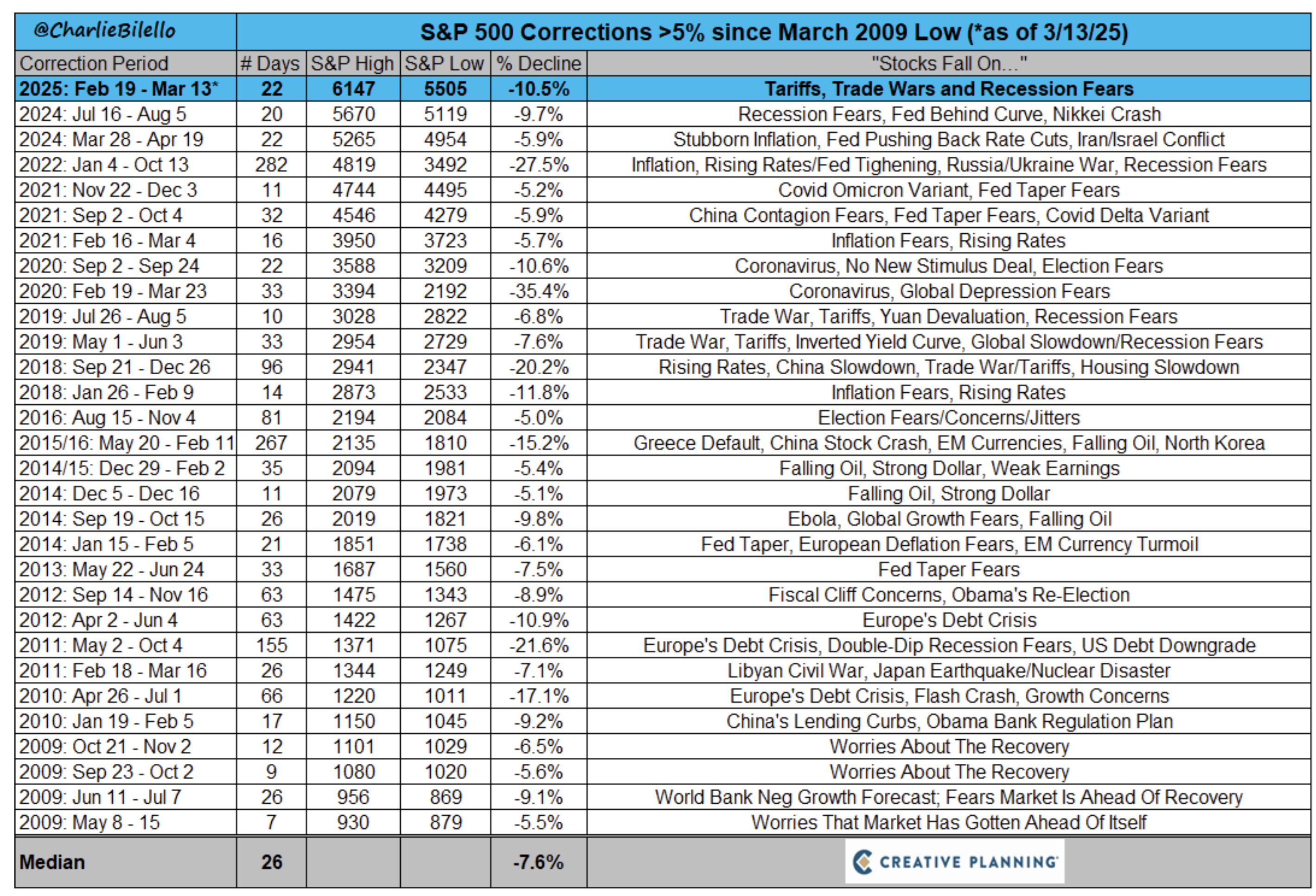

Retirement Roundup - March 21, 2025

Retirement Roundup - March 7, 2025

Retirement Roundup - February 28, 2025

2024 Market Overview

Retirement Roundup - February 21, 2025

Retirement Roundup - Friday February 16, 2025

Top 3 Areas Retirees Struggle at the Beginning of Retirement

Most working Canadians look forward to retirement. The day that they can turn in their laptop, work tools, and security access cards and transition into a life of relaxation and free time is one that gets most people excited. And for good reason. Retirees typically have more time to live life on their terms with way more time to do it without work getting in the way. But, the transition from working life into retirement isn't always perfectly smooth. Having had a front row seat to a lot of new retirements, I have had a chance to see what works well for people and areas where they struggle. Here is a list of the 3 biggest areas where I've seen new retirees struggle.

How Much Does Long Term Care Cost in Ontario?

The cost of a long-term illness or other health condition that will require an extended stay in a long-term care facilities is one of, if not the largest unknown expense that a retiree may encounter as they age. According to the Long Term Care Association, 1 in 5 seniors over the age of 80 has a complex healthcare need that can only safely be met in a long-term care facility. And according to Statista from survey data gathered in 2021 - 40% of long term care stays are between 1 and 3 years, 21% are between 3 and 5 years, and 14% of stays are greater than 5 years. While many seniors may be fortunate enough to avoid needing enhanced care services in retirement - the risk is still significant enough that retirees should be discussing how they would respond in the event that the need for this type of care arises. In this video we will cover the health conditions that may necessitate a stay in long term care, the different types and levels of long-term care support in Canada and their associated costs, and how retirees should be planning for the potential costs and lifestyle impact that a move to long-term care will bring.