Factor Investing Part 4 - Term and Credit Premiums in Fixed Income

When thinking about long-term investing, we typically think about stocks or the stock market. Most of financial journalism and popular media focus on famous stock pickers, stock benchmarks, and company stock prices.

The often-forgotten, but nevertheless critical asset class for many investors is fixed income which are broadly referred to as bonds. Stock holders are owners of the company and are entitled to a share of dividends that are paid out if the company issues them or if the company itself is ultimately liquidated. Bond holders are lenders of capital to the company or, in the case of government bonds, the government.

In exchange for the cash that they lend, investors are entitled to regular interest payments and the return of their original investment at the end of the bond's term. In the case of corporate bonds, that promise is secured by the assets of the company. So if a business goes bankrupt, the bondholders are first in line to get their money back before the stock holders receive anything. In the case of government bonds, the bonds are backed by the promise and its ability of that government to pay its debts via powers of taxation.

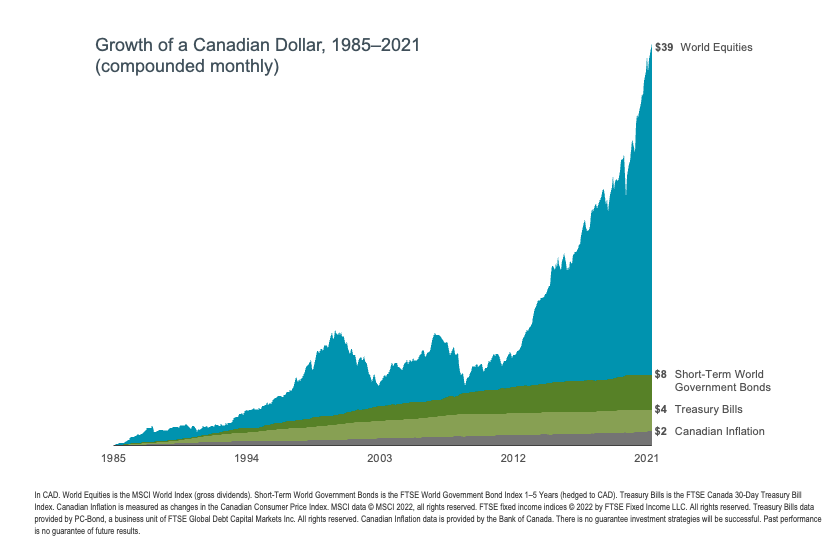

For these reasons, by and large, bonds are less risky than stocks. This is evident when looking at the returns of a dollar invested in a portfolio of global equities when compared to a portfolio of government bonds since 1985.

What are Bonds for?

If bonds have lower returns than stocks - why would we want to own them in our investment portfolios? Ultimately it comes down to matching your investment portfolio with your financial plan.

Because they are less risky, bonds can be deployed for things like covering near-term spending needs. Provided that the term of the bond is aligned with the timeline of the spending goal, an investor can generate positive returns without exposing themselves to the much higher volatility of stocks.

For investors who do not need or want to take on the additional risk and volatility of owning all stocks in their investment portfolios, bonds have historically done a good job of "smoothing" the ride out for those investors. Higher allocations of fixed income tend to reduce long-term returns, but they also reduce short term volatility along the way, while still providing positive returns. For investors who are drawing regular income payments from their portfolio, reducing volatility is an important part of making sure that the portfolio can sustain itself over the long run. Of course, we want an income portfolio to grow over a decades-long retirement, but we also need to avoid a situation where the portfolio is depleted too quickly during a temporary downturn in stock prices.

To help illustrate, here is a chart showing some historical model portfolios of different stock and bond combinations.

What Drives Bond Returns?

While bonds are generally less risky than equities, there are still differences in expected returns for different types of bonds. They are, in my opinion, much simpler to grasp and intuitive - which is why there is only one blog post in this series dedicated to fixed income :).

The two "factors" that explain the differences in bond returns are:

1) Term Factor - longer term bonds have, historically, provided higher returns than shorter term bonds.

The simple risk-based explanation for the term premium is that investors demand a premium for accepting the risk of higher inflation in the future, and more volatility in interest rates over long periods of time.

To simplify this, consider you have $10,000 to invest in a bond. One bond is offering a 3% coupon for 3 years (we will use interest rate as the proxy for coupon to keep it simple). Another bond is offering a 3% interest rate for 5 years. Even though the rate is the same, you decide to go with the 5 year bond. After all, it's 2 more years of getting interest payments and you don't think you'll need the money in the interim. So, you're ok with this purchase.

But, are you taking into account the fact that interest rates may change over this longer time period? What if inflation is higher than expected? Your money is now locked into this bond for 5 years instead of 3. You are taking more term risk by owning the 5 year bond vs. owning the 3 year bond.

Generally, investors in longer term bonds will demand a higher return than investors in shorter term bonds. That is the term factor.

To help illustrate the term factor, here is a comparison between 1 month Canadian treasury bills and the 1-5 Year Canadian Government Bond Index.

2) Credit Factor - lower credit quality bonds (ie. corporate bonds) have, historically, provided higher returns than higher credit quality bonds (ie. government bonds).

A simple risk-based explanation for the credit factor is that investors will demand a higher return for accepting the higher risk of default of a lower credit quality issuer (ie. a large corporation) than they will for similar duration bonds from a higher credit quality issuer (ie. a government bond issuer).

Going back to our example above, let's say you have the choice between a large Canadian telecommunications company bond paying 3% interest for 3 years, and a Government of Canada bond paying 3% interest for 3 years. Are you indifferent between them because they are paying the same interest rate? Chances are, you will prefer to own the Government of Canada bond. While it is not likely that the large Canadian telecommunications company is going to default on that debt inside of the next 3 years, it is certainly more likely than the Canadian government defaulting on its debt.

To help illustrate the credit factor, here is a comparison between the Bloomberg US Government Bond Index and the Bloomberg US Corporate Bond Index.

Conclusion

This brings our introduction to Factor Series to a close! I hope you found it helpful.

To recap, here is a list of the factors we covered with links to previous articles:

1. Market risk - the higher risks we take and returns we expect from holding stocks vs. holding treasury bills over long periods of time

2. Size risk - the higher risks that we take and returns we expect from favouring smaller company stocks vs. larger company stocks over long periods of time.

3. Relative price risk - the higher risk that we take and returns expected for favouring relatively cheap stocks vs. relatively expensive stocks over the long run

4. Term and Credit risk - the higher risks that we take and returns we expect for favouring relatively longer-term bonds vs. shorter term bonds and relatively poorer credit quality bonds vs. higher credit quality bonds.

Make sure to check back in if you'd like to read more articles on evidence-based investing and financial planning for Canadians. Or, you can subscribe to my weekly video newsletter here:

Thanks for reading!

--

The comments contained herein are a general discussion of certain issues intended as general information only and should not be relied upon as tax or legal advice. Please obtain independent professional advice, in the context of your particular circumstances. This article was written, designed and produced by Mark Walhout, CFP®, an Investment Funds Advisor with Investia Financial Services Inc., and does not necessarily reflect the opinion of Investia Financial Services Inc.The information contained in this article comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any securities.

Mutual Funds are offered through Investia Financial Services Inc. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.