What Kind of Retirement Can I Expect with $1 Million Dollars Saved Up?

The most common retirement savings assumption that I hear is that you need about $1M saved up to retire comfortably.

Can you comfortably retire with $1M saved up? It depends.

I thought it would be a fun exercise to model out a $1M retirement for a hypothetical couple - Jack and Jill. There are so many unique situations that limit the usefulness of examples like these, but I'd like to help you out with a reference point for this question.

Before we get into the results, let's start with a few assumptions. I have tried to keep the assumptions as simple as possible.

Assumptions

Age - I have assumed that our hypothetical couple is exactly 65 years old and plans to retire in January 2022.

Income - They each earn $100,000 per year, and have been saving $1000 per month each into RRSP's.

Life Expectancy - I have assumed that moth members of the couple are going to live until exactly age 100.

Savings - The couple has $1M in retirement savings today (November 9) allocated as follows:

- $400,000 in an RRSP for each member of the couple

- $100,000 in a TFSA for each member of the couple

Emergency Fund - They also have an emergency fund outside of this retirement nest egg. I recommend a fund large enough to cover at least one or two major house repairs and enough to pay for any major capital purchases you have coming up in the next 3-5 years (ie. new car).

Investment Portfolio - I have assumed that the couple has their entire portfolio allocated to a global 60% stock, 40% fixed income portfolio.

Return Assumptions - I have assumed that the return of the stock/bond portfolio will be 4.68% for the life of the plan.

Product and Advice Fees - I have assumed that their total investment product and advice fees are 0.88% per year, calculated as a percentage of their investment portfolio.

CPP and OAS - I have assumed that each member of the couple will get 80% of the maximum of CPP (Canada Pension Plan), and 100% of the maximum of OAS (Old Age Security). For simplicity, I assumed they would begin taking these benefits when they retire.

Home - I have assumed that the couple owns a $1M home, with no plans to downsize. They live in Ontario (for income tax purposes)

Inflation - I have assumed that inflation will be 2% for the life of the plan.

Software - I used Navi Plan for this plan and Monte Carlo simulations.

(I will talk more about long-term assumptions at the end of the show)

Initial Results - How Far Does $1Million in Retirement Savings Go?

After inputting this information, and solving for how much after-tax retirement income this couple could expect - here were the initial results.

Sustainable Lifetime Income - $6,000 per month after-taxes, for life

Based on the assumptions above, our couple could expect to be able to generate an after-tax income of $6,000 per month after taxes for the rest of their life.

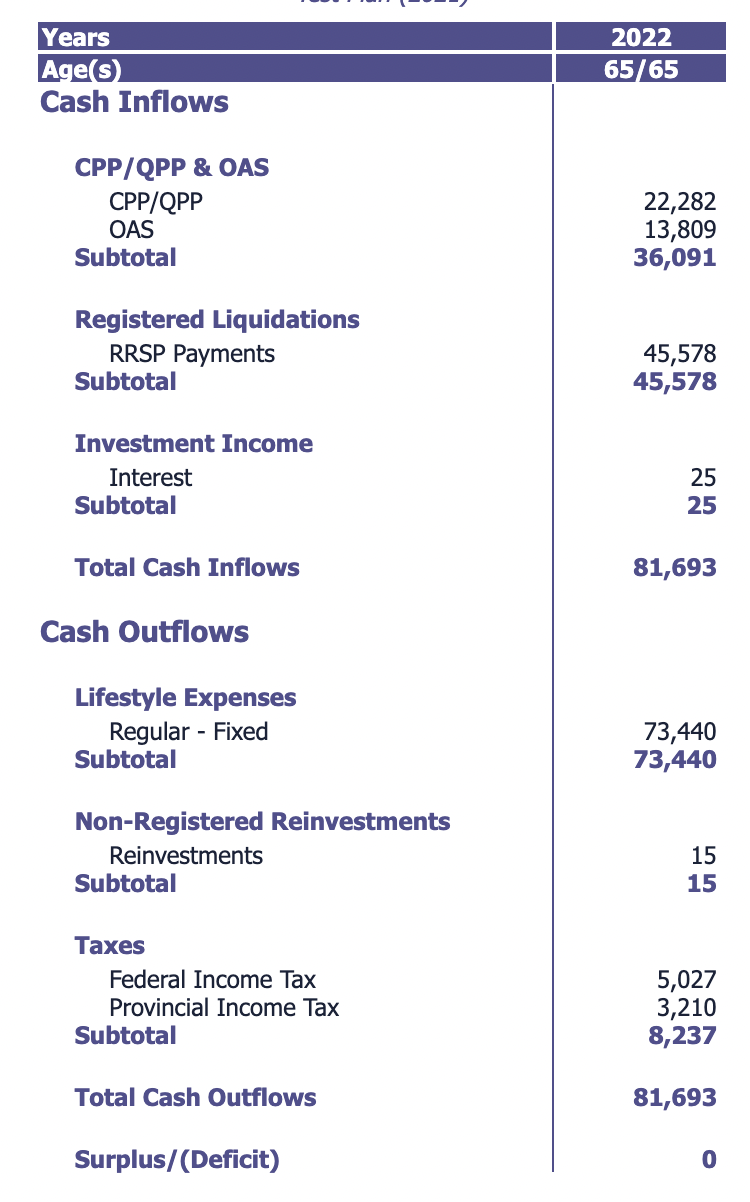

Here is a snapshot of their first year retirement budget (pulled from Navi Plan)

As you can see, CPP and OAS make up a pretty significant portion of their retirement income (close to half). For those who enjoy withdrawal rate rules, at a $45,578 withdrawal is around a 4.5% first year withdrawal rate.

Potential Issues

While the projection shows that the retirement plan is successful, this assumes a nice and smooth set of returns throughout retirement. As we know, investment returns are not always so smooth. For people who are preparing to generate income from their investments, this is known as sequence risk.

The best way to illustrate sequence risk is with a simple example. In both sequences, $100 is invested at the beginning of year 1.

|

|

Return Sequence 1 | Return Sequence 2 |

| Year 1 | - 14% | 5% |

| Year 2 | +15% | 5% |

| Year 3 | -3% | 5% |

| Year 4 | +14% | 5% |

| Year 5 | +13% | 5% |

| Total after 5 years | $123.58 | $127.63 |

The average return over these 5 years was the same, but the volatility of the portfolio and the sequence that the returns come in makes a difference. In this simple example, the first year of returns was bad, and even though the annual returns in 3 of the next 4 years were substantially higher than the average return, it couldn't make up for the shortfall. If you imagine also taking an income from the portfolio while these volatile returns are occurring, a retirement can go sideways in a hurry.

In the case of our simple $1M retirement and 4.5% initial withdrawal rate, we can model out the potential impact of this sequence risk using a Monte Carlo simulator. The simulator basically models a set number of random sequences of returns against the financial plan and see how the portfolio fares using the assumptions we listed above. The inputs for the Monte Carlo simulator are the assumed long range average return and the assumed volatility (measured by standard deviation).

In the case of this sample $1M retirement plan, the simulator told us that this plan was successful in about half of the simulations run. This means that the couple may run out of money if they experience a bad return sequence early in retirement.

This is NOT the same as FORECASTING that they WILL run out of money. A Monte Carlo simulator is not a forecasting tool.

It simply acknowledges that withdrawing from a volatile portfolio of assets carries risks. Therefore, we need to be prepared to adjust to this situation if it comes up.

Also note that we have an equal chance of having great returns early, which would mean that they can increase their spending as retirement goes on. This is part of the reason why it is important to keep financial plans updated as retirements progress.

Spend a Little Less Now to Avoid More Painful Cuts Later

To combat this, I modelled out reducing their spending by about 10% to start retirement. So, instead of spending $6,000 after-tax for life, we will start them out spending $5,400 per month for life. This reduced their portfolio withdrawals in the first year of retirement from $45,000 to around $36,000 - or about a 3.6% initial withdrawal rate.

Here is the comparison of the Monte Carlo scenarios - $6,000 monthly spending on the left, $5,400 monthly spending on the right. As you can see, starting out with a lower spending level pushes our 10% scenario (close to worst case) further out. This means that in the worst case scenario, if this hypothetical couple kept withdrawing the same amount adjusted for inflation to cover their $5,400/mth after-tax retirement needs, and ignored what was happening in the market completely, the earliest they would deplete their portfolio is 2049, or about age 93.

Note, this is an issue of preference and is unique to each person's situation. You may be ok with running the risk that you may need to cut your spending as your retirement progresses, and therefore be ok with starting with a slightly higher withdrawal rate. You don't necessarily NEED to have a Monte Carlo result that shows 100% success rates through all market conditions.

If I was advising you, I would ask you to specifically tell me which expenses you were prepared to cut in the event that such a cut was necessary. If the income plan was already "cut to the bone" so to speak, we would have to discuss other strategies with this hypothetical couple. Perhaps they would consider downsizing their home later in retirement, some part time work early in retirement, delaying retirement, or some combination of these.

But, Mark, I Want to Spend More

If our hypothetical couple doesn't like this plan and want to spend more, there are some things that they can do to improve their income plan. The main ones that make a big difference for retirees is either finding a way to increase their income, or finding a way to turn other assets on their balance sheet into income.

As I stated in the assumptions, I did not model out downsizing the home for Jack and Jill in this example. The "if-this-then-that" scenario creation is very, very unique to each individual couple and I didn't think it would help you for the purposes of this podcast episode.

Let's just suffice to say that if this couple wanted to access some tax-free capital to supplement their retirement income, or their healthcare spending needs later in retirement, they have access to the equity in their home. They can access this via a line of credit, or a reverse mortgage as well if they love their home and they would prefer not to move.

Back to our couple. They want to spend about another $20k per year after taxes on exciting trips and travel while they are healthy and active. They expect that this will be for at least the first 10 years of their retirement. This represents about a 25% increase in spending for the early phase of retirement. Assuming that our hypothetical couple isn't comfortable with tapping into home equity - what are their options?

Jack and Jill Make Some Adjustments

I modelled out a couple of moves that our couple can make that will get them into the travel that they want to do.

1) Work a bit longer - I modelled out our couple working for 2 more years full time. Yes, 2 years is a meaningful amount of time to stay working when you want to retire. But for the chance to travel to Fiji, Australia, and across Europe over the next 10 years, Jack and Jill believe it is worth it. We also pushed out their CPP/OAS collection dates until age 67 (their new retirement date).

2) A little bit of part time work - I modelled out our couple doing some part time work for the first 3 years of retirement, about $15,000 each. Ideally, this couple can do some lite consulting in their field. Alternately, even a moderately paid part time jobs should be able to boost their income by about $30,000 per year for 3 years in their early retirement.

3) A bit more saving - I have assumed that they will continue their $1,000/mth each saving for the next 2 years until they retire. The combined forces of a) saving for longer b) investments growing for longer c) investments not being drawn off of for longer and d) investments needing to fund a shorter retirement are MASSIVE tail winds to a retirement plan.

These 3 moves make their additional spending for the first 10 years of retirement achievable for them.

Below is a cashflow projection for the first 10 years of their retirement (showing every other year for brevity), reflecting the changes we made above:

When we stress tested this scenario using the Monte Carlo Simulator, we get great results for this alternative.

Bringing it All Together

In our example, Jack and Jill can create a sustainable withdrawal of about $35,000 per year from a portfolio of $1M invested in a 60/40 portfolio.

When combined with CPP/OAS, their achievable income goes to about $5,400/mth after tax, adjusted for inflation, for life.

If they are prepared to work a bit longer and do some part time work in retirement, they can increase their spending in the first 10 years of retirement significantly.

Here are just some of the caveats that could change this outcome for Jack and Jill, or another couple approaching retirement:

- Life Expectancy - I have assumed Jack and Jill will each live to 100 - if they have a shortened life expectancy, that may increase their sustainable spending rate, but it may also necessitate that we plan for higher healthcare costs down the road.

- Retirement Date - Jack and Jill are planning to retire at age 65, but a lot of people retire earlier or are "retired" by their employer earlier than they expect. For people retiring early, their starting withdrawal rate will likely need to be lower than what I have modelled here. Unless, of course, they are prepared to make spending adjustments as their retirement progresses.

- CPP/OAS - As you can see, CPP and OAS make a up a big part of Jack and Jill's retirement plan. If you are within 10 years of retirement, it is a good idea to get an estimate for your CPP entitlement from Service Canada so that you set your expectations properly for your entitlement. If you were out of the workforce for many years, earned income lower than $60,000 CAD on average during your career, paid yourself only in dividends from a private corporation and did not contribute to CPP during that time - you may have a substantially lower CPP entitlement. Also, if you are a relative newcomer to Canada, you may also have a lower OAS entitlement. Do not simply assume that you will be getting the maximum CPP/OAS benefit.

- CPP/OAS timing - in this simple example, I assumed that Jack and Jill would begin taking CPP/OAS the moment they retired. They may benefit from taking at least CPP later (as late as age 70) and increasing their lifetime inflation-adjusted benefit.

- RRSP/TFSA/Non-Registered Mix Makes a difference - I assumed that Jack and Jill had $200k of their portfolio in TFSA's and $800k in RRSP's. This will have made the back end of their retirement much more affordable because of the tax-free compounding and tax-free withdrawals that they will enjoy when their RRSP/RRIF accounts draw down in the middle of their retirement. If you have a different proportion of your savings in RRSP/TFSA/non-registered accounts, it will impact your tax situation in retirement as well as your sustainable retirement income

Conclusion

I have never had a client approach me with a situation this clean and simple :). People have second properties, rental properties, pensions, company stock, passive income, dependant children, dependant parents, one-spouse much older than the other spouse...the list goes on!

For some people, $1 million in retirement savings will be more than they will ever need. For others, it will not be nearly enough. I encourage you to speak with a financial planner to help you map out a customized retirement income plan that is designed for you.