Co-Signing on Children's Mortgages & Government Debt and Stock Returns

Co Signing on a Child's Mortgage

On today's episode, I am going to cover a question that I received from a couple of clients over the past month. Whenever I receive the same question twice inside of a month, I take that as a sign that it is worth creating a podcast episode to talk about it.

The question is around co-signing for a child's mortgage. Increasingly, parents are helping their children fund the purchase of houses.

According to a report from CIBC, released in October of this year, over 30% of home buyers got help with their purchases from family members. For first-time home buyers who received , the average gift that they received was $128,000.

But, not all families need or want to make a major lump sum cash gift to their children to buy a house.

The other way that children are reaching out to their families to help them qualify for a mortgage is by asking them to either co-sign or guarantee their mortgage.

A lender may ask a borrower for a co-signor if they have limited or questionable credit history, or their income is at a level where the bank asks for more assurances.

A special note here - I am a member of a financial planning group called the Financial Planning Association of Canada (FPAC). When this question came up, I put it to the member forum. The content of my answer is, in large part, a collection of their helpful responses to me.

For any financial planners who are listening to this podcast, I highly recommend joining FPAC, or attending a membership event. (links below).

Becoming a co-signer will have some implications for you as a parent:

- You will be fully liable for the child's mortgage debt. This means that if your child has issues with the payments, you will be fully on the hook for payments as the co-signer.

- Being co-signer will limit your ability to borrow. You will need to disclose to potential lenders that you are co-signed on a child's mortgage and that will reduce your borrowing capacity.

- There may be income tax implications for being a co-signer. As co-signer, your name may need to go on the title as a legal owner of the house. If your child sells the house down the road, they will be able to access the Capital Gain Exemption so that they don’t need to pay taxes on that sale. But, if you are a co-signer on the mortgage, you *may* have to report a capital gain on your “portion” of the house when it sells.

If you need to go on title, you may want to speak with a lawyer about setting up what’s called a “Declaration of Trust”. This document will make clear several things between you and your child:

- Your child is the sole beneficial owner of the property

- Your child is responsible for all costs (capital and maintenance) of the property

- You (parent) cannot mortgage the property or use it as a security for another loan

- All tax obligations for the sale of the property in the future belong to your child

- In the event that your child pre-deceases you, the home will go into your child's estate fully (not yours)

- If you pre-decease your child, your “share” will be held in trust for your child

Basically, this document should “distance” you entirely from any tax consequences that may arise for you due to you being on title. It spells out clearly and acts as proof to the CRA that the beneficial ownership of the property, and any resulting tax consequences, rests entirely with your child.

As a backup, when your lawyer/child's lawyer is drafting the deed of the house, you can ask that they put you (the parent) down as a 1% owner only. That means that, in the event of a sale, at worst only 1% of the gain on the sale of the house will be taxed in the hands of the parent.

Please note, this agreement does NOT nullify your other obligations/risks listed above. You will still be on the hook for the debt if something goes wrong, and it will limit your future borrowing capacity.

Government Debt and Stock Returns

Governments in developed markets all over the world have been expanding their borrowing significantly over the past 2 years. Money has been borrowed to send money to people impacted by the COVID-19 pandemic. Money is also being borrowed to stimulate economies as we (hopefully) emerge from the pandemic.

Investors may be wondering if they should adjust their asset allocation by country, depending on the debt level of that country. Or, more simply, they are asking the question - Does a high-debt country's stock returns suffer when compared to a low-debt country? There have been studies done in the past that have argued that debt financed government spending may cause interest rates to rise or crowd out private spending. Others that have argued that the supply of public debt instruments may discourage investors from investing in private businesses and private debt.

Dimensional Fund Advisors released a paper last week that looks at the historical data and brings some light to these questions.

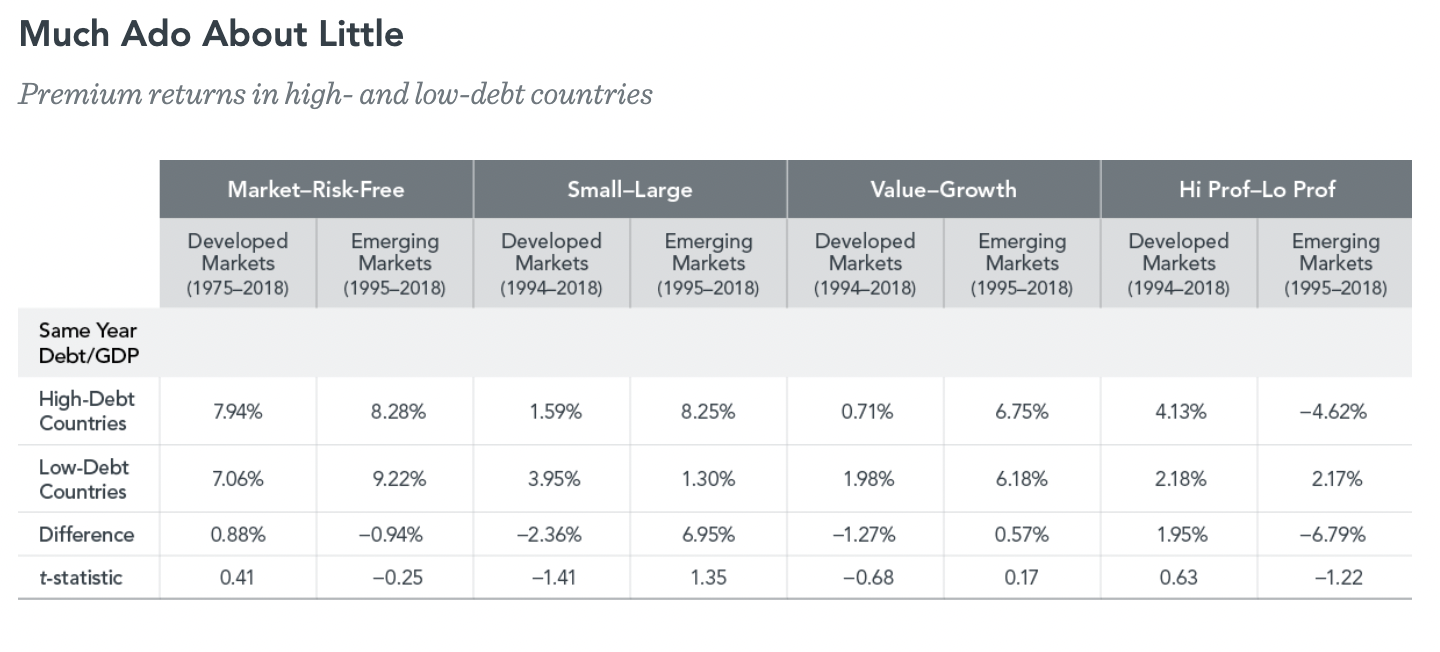

First, they looked at the number of countries that have high debt. The paper revealed that half of the Organization of Economic Co-Operation and Development (OECD) member countries have general government debt-to-gross domestic product (Debt/GDP) ratios over 70%, with 10 countries with Debt/GDP ratios exceeding 100% of GDP (including Canada, US, Japan, and the UK).

From there, the paper looked at some scenarios:

1. Compared high-debt countries as a group to low-debt countries as a group and compared their stock/bond market returns and found no statistically reliable difference between them. The study looked at each country's debt/GDP ratio on a year to year basis from 1975 through the end of 2018. If a country landed above the median debt/GDP threshold, it was put in the "high debt" group. If it was below, it was put in the "low debt" group. Surprisingly, there was no reliable relationship between high debt countries having lower stock returns than lower debt countries.

2. From there, the paper looked at the direction of debt. Said differently, they looked at countries whose debt was rising at a fast rate year over year vs countries whose debt was rising at a slower rate year over year. Once again, there was not a statistically significant difference to be found.

1. High debt doesn't necessarily forecast impending default - Japan has had debt/GDP levels above 200% for more than a decade without default. Argentina defaulted on its government debt in 2019 with debt/GDP of only 90%. Ivory Coast defaulted in 2011 when its Debt/GDP was just 46%.

2. Debt is a slow-moving variable - market participants buying and selling stocks have a lot of time to reflect expectations about debt levels in stock and bond prices. Debt crises don't, generally, "pop up" overnight.

3. Power of Market Prices - it can be argued that the lack of relationship between country debt and stock market returns could signify that debt affects drivers of stock returns in ways that ultimately offset one another. Meaning, market participants are anticipating the positive (ie, more demand) and negative impacts (ie, potential higher debt servicing costs down the road) of debt as they set prices for securities.

Resources

dimensional.com/ca-en/insights/government-debt-and-stock-returns