28. Is Gold a Great Investment for Retirement? And, How to reduce taxes and probate for your estate

Welcome to Episode 28 of Retire Me!

On today's episode, we explore gold and its value to a retiree portfolio. We also talk about ways to reduce taxes and probate when planning your estate.

Gold

There are 3 main arguments that are held out for owning gold in your investment portfolio. I explore each one with data that I was able to pull from www.portfoliovisualizer.com. This is a free tool that you can use yourself if you are interested in comparing performance of different portfolios and even running your own Monte Carlo simulations. I also include some charts from DFA returns web.

3 main arguments for holding gold

1. It is a good hedge against inflation

Gold advocates argue that gold is a good hedge against inflation. Historically, they are correct - Gold is a good hedge against inflation historically.

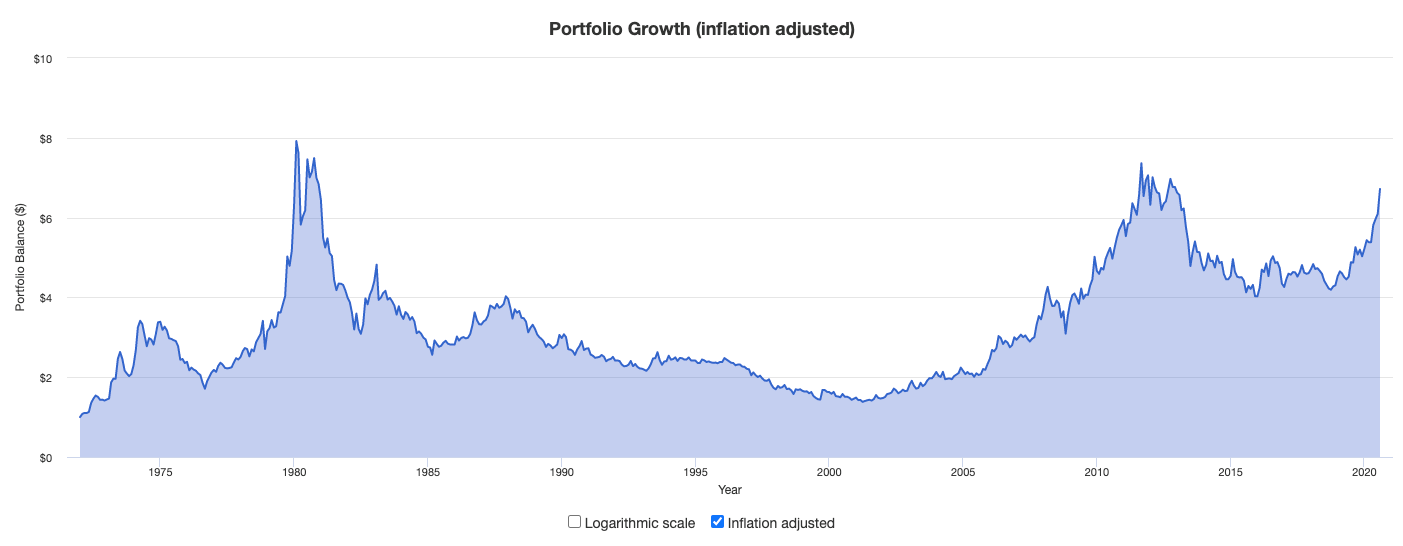

Below is a chart showing the inflation-adjusted performance of gold since 1972 (the earliest that portfoliovisualizer would let me go back). $1 invested in gold in 1972 would be worth about $7 in 2020 dollars. That's a pretty good hedge against inflation in the long run.

But, as you can see, there are long stretches where, on an inflation-adjusted basis, gold massively underperformed inflation during that time period. Take for example the period of time between 1980 and 2002. $1000 invested in gold in 1980 would have been worth only $288 in 2002 on an inflation adjusted basis. See below:

So yes, gold over very long stretches of time is a good inflation hedge historically. But, over significant periods (in this case 20 years), gold can massively underperform inflation and the value of an investment in gold can lose a lot of its value. Since retirements can last between 30 and 40 years, having a significant portion of your retirement portfolio losing that much value against inflation is not an acceptable outcome to most people.

2. Gold is good to hold when the world is falling apart

Gold proponents argue that gold is a stable asset to hold during bear markets. Larry Swedroe writes

As for gold serving as a safe haven, meaning that it is stable during bear markets in stocks, Erb and Harvey found gold wasn’t quite the excellent hedge some might think. It turns out 17% of monthly stock returns fall into the category where gold is dropping at the same time stocks post negative returns. If gold acts as a true safe haven, then we would expect very few, if any, such observations. Still, 83% of the time on the right side isn’t a bad record.

So, not a bad argument here. Roughly 4 times out of 5, gold has gone up when stocks have gone down on a monthly basis.

3. Gold is negatively correlated with stocks, and therefore it is a strong diversifier

This is sort of the same argument as above, so I apologize if it's redundant. In the chart below I measure the return of US stocks and the return of gold going back to 1972. A couple of observations:

1) The correlation of gold and stocks, since 1972 has actually been 0.02, which means that there is no relationship between the price movements of gold and US stocks over that time period. So, it can be a good diversifier in that it moves independently from stocks, but it doesn't move opposite to stocks

2) The annualized return of stocks vs. gold measured by the Compound Annualized Growth Rate (CAGR) is 29% higher than the returns of gold with 22% less volatility.

Summary

Gold has a lot of appeal these days because the values of gold and gold mining stocks have been going up. It also has a lot of emotional appeal for investors in many of the same ways that real estate does. It is tangible and people have a strong emotional connection to it (we give gold as gifts, after all).

The arguments for holding gold that I believe hold water are:

1) it is a diversifier in that it is not correlated with stocks (see above)

2) a small holding in gold that keeps you invested in your main portfolio of stocks and bonds is a reasonable amount (5%)

My main arguements against holding gold are:

1) It is very volatile - so, if you invest a significant amount in gold and watch it fall and stay down for a long time, are you prepared to stick with it? If not, and you will bail out of the investment after a possibly very long period of underperformance (see above), then you should avoid it.

2) If you want to improve your returns and lower your volatility there are other things that I recommend you do first - have you invested in small cap stocks, value stocks, more profitable companies? Have you diversified your portfolio globally?

As an example, take a look at two 60% equity/40% fixed income portfolios. A 60/40 is a good proxy for what a retiree portfolio could look like.

One portfolio is made up of Canadian stocks and Canadian Bonds.

The other portfolio is diversified with US and International stocks and bonds, with a tilt towards small cap/value/profitable stocks. This is the 60/40 portfolio that I use with my clients. The returns are similar, but the diversification that we added in with the Dimensional portfolio reduced the volatilty by 1/4.

So, for clients who are interested in gold, I would suggest first making sure you've diversified well enough with investments that have more reliable expected future returns. Gold can provide a diversification benefit, but it is wildly volatile and cannot be relied upon to deliver positive returns for retirees if it is held as a large proportion of the wealth you expect to live on in retirement.

Reducing Taxes and Probate

Tax Tips Link to Probate Fees In Canada

--

Disclaimer - This podcast is for informational purposes only. Please consult with a financial advisor familiar with your unique financial situation before making any decisions. Nothing in this broadcast constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns. Mark Walhout is the owner and lead financial advisor at Walhout Financial and an Investment Fund Representative at Investia Financial Services Inc.